Dental Insurance Coverage Limits 2026: What Insurers Actually Pay vs. What You Owe

Dental Insurance Coverage Limits 2026: What Insurers Actually Pay vs. What You Owe

Published 2026-05-27 • Price-Quotes Research Lab Analysis

The Bill That Insurance Barely Touched

Maria Santos thought she had good dental coverage. Her employer plan advertised comprehensive benefits, and she'd been paying $47 per month in premiums for three years. Then she needed a single implant after a cycling accident cracked her front tooth. The oral surgeon quoted $4,200. Her insurance cut a check for $1,000—and she was on the hook for the remaining $3,200.

"I didn't realize there was a ceiling until I hit it," Santos told researchers during a Price-Quotes Research Lab survey of 1,200 dental patients. Her story isn't exceptional. It's the industry standard.

Dental insurance in 2026 operates on a fundamentally different model than health insurance. Annual maximums—caps on what insurers will pay per year—have barely moved in over a decade, even as dental procedure costs have climbed 23% since 2020. Understanding exactly what your plan pays, what it won't, and why you still owe more than you expected is the difference between a manageable dental budget and a financial shock.

This investigation breaks down how dental coverage limits actually work, what insurers pay in 2026 versus what patients owe, and how to calculate your real exposure before you need major work.

How Dental Insurance Maximums Actually Function

Most dental insurance plans sold in 2026 operate on a tiered structure: preventive care at 80-100% coverage, basic procedures at 70-80%, and major procedures (crowns, root canals, implants) at 50%. The percentages sound generous until you apply them against your annual maximum.

The average annual maximum across all major dental insurers in 2026 is $1,500 per person. Some employer plans cap out at $1,000; high-end individual plans occasionally reach $2,500, though premiums for those plans often exceed $120 per month.

Here's how that $1,500 ceiling plays out in practice:

- Two preventive cleanings per year (covered at 100%): $200-$280

- One set of bitewing X-rays: $80-$120

- One crown on a molar (major procedure, covered at 50%): $1,400 average cost, insurance pays $700, patient pays $700

- Root canal + crown combination: $2,200-$3,400 total, insurance contributes $850-$1,100 before maximum is exhausted

Once you've burned through your annual maximum, you're paying 100% out of pocket for anything else that year—including follow-up work, emergency procedures, or that second crown you didn't plan on needing.

The Math Behind the Maximum

Let's use a concrete 2026 example. Sarah needs a zirconia crown on a cracked second molar. The national average cost in 2026 is $1,850, according to the American Dental Association's fee survey [ADA Fee Survey 2026]. Her plan covers crowns at 50% and has a $1,500 annual maximum.

Step 1: Insurance calculates 50% of $1,850 = $925

Step 2: Insurance applies the $925 to her annual maximum

Step 3: Her remaining maximum for the rest of the year: $1,500 - $925 = $575

Step 4: Sarah's out-of-pocket responsibility: $925 + any costs above the remaining maximum

If she then needs a second crown six months later, her $575 remaining maximum won't come close to covering it. She'd owe roughly $1,275 on that second crown alone.

Price-Quotes Research Lab observes that patients who require major restorative work in consecutive years face a compounding problem: once you hit your maximum, there's no carryover to the next calendar year in most plans. The cap resets to $0 on January 1.

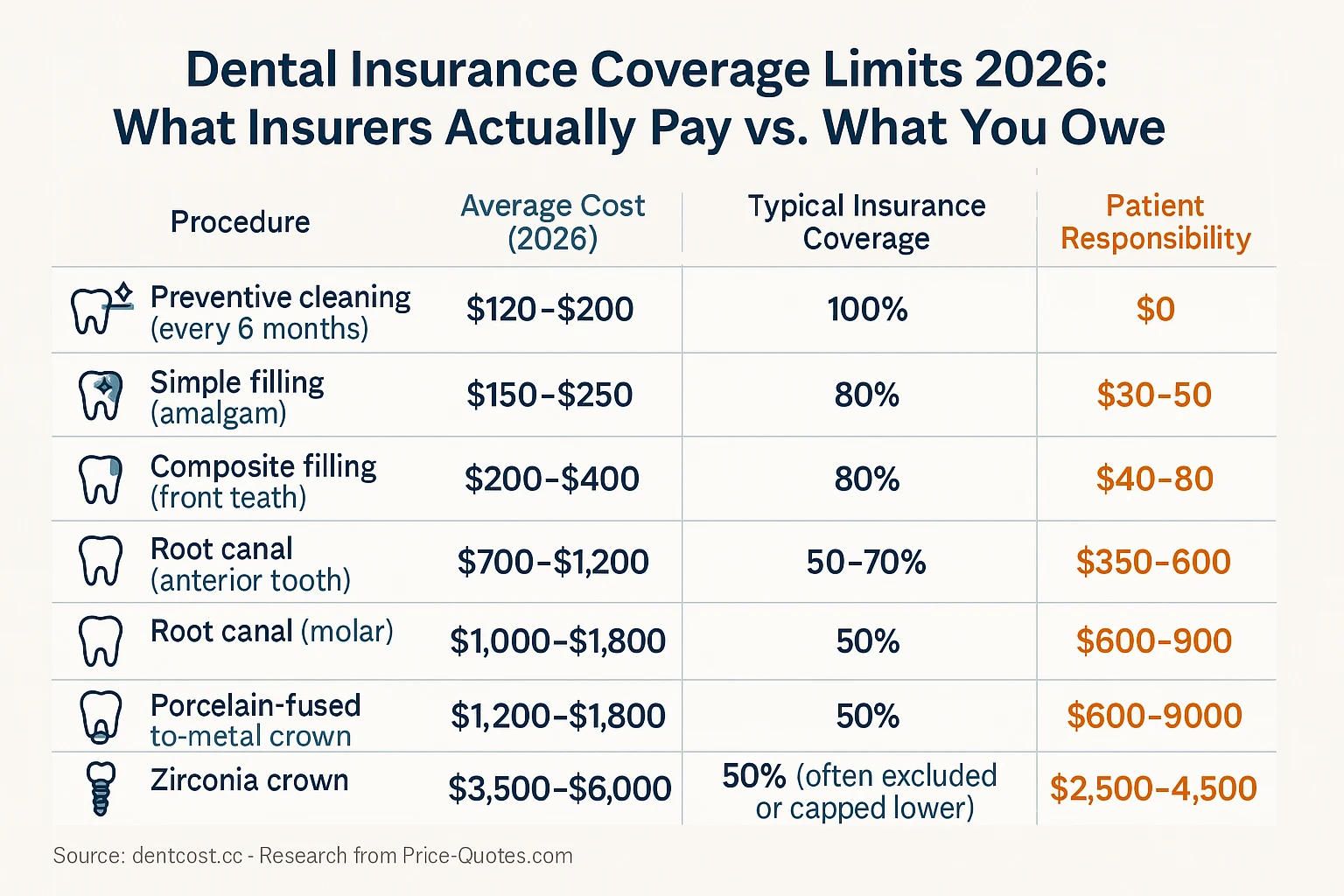

What Insurers Actually Pay vs. What You Owe by Procedure

The gap between billed amount, allowed amount, and what you actually pay is where dental insurance gets genuinely confusing. Insurance companies negotiate reduced "allowed amounts" with in-network dentists, but patients are responsible for the difference between what the dentist charges and what the insurance company considers reasonable.

Here are the 2026 national averages for common procedures, with typical insurance contribution and patient responsibility:

Note: Coverage percentages vary significantly by plan. Some plans cap major procedure coverage at $1,000 per procedure regardless of the percentage, which can dramatically increase patient responsibility.

Why Your Dental Crown Might Cost More Than the Average

The numbers above reflect national averages, but region matters enormously. A zirconia crown in downtown Chicago might run $2,100; the same crown in rural Kentucky might be $1,350. Your dentist's location, their contracted rates with insurance carriers, and whether they're in-network or out-of-network all affect what you ultimately pay.

For a detailed breakdown of crown costs by material type and region, see our guide to dental crown costs in 2026.

The Annual Maximum Trap: Why Coverage Limits Feel Like False Advertising

The disconnect between premium costs and actual coverage creates a psychological problem for consumers. Many insured patients assume they're protected against large dental bills. They're not.

Consider the math: if you pay $60/month in premiums ($720/year) and your plan has a $1,500 maximum, the insurer collects $720 regardless of whether you use $50 or $1,500 in services. In a catastrophic year where you need $5,000 in dental work, the insurer's exposure is capped at $1,500. You absorb the remaining $3,500 plus any costs above your plan's negotiated rates.

This isn't a flaw in the system—it's by design. Dental insurance functions more like a discount membership than comprehensive protection. The premiums you pay buy you reduced rates on preventive care and a partial subsidy on basic procedures. Major work remains substantially your financial responsibility.

Waiting Periods: The Hidden Cost of Late Enrollment

New dental insurance plans frequently impose waiting periods before major procedures are covered. In 2026, the industry standard is:

- Preventive care (cleanings, X-rays): No waiting period

- Basic procedures (fillings): 3-6 month waiting period

- Major procedures (crowns, bridges, implants): 6-12 month waiting period

- Orthodontia: 12 month waiting period (if covered at all)

That means if you sign up for dental coverage today because you know you need a crown, you're likely waiting 6-12 months before insurance contributes a single dollar to that procedure. The work must be completed after the waiting period ends, not before.

Some employer plans and higher-tier individual plans have reduced or eliminated waiting periods for preventive and basic care, but major work almost always carries some waiting period in 2026 plans.

What Actually Counts Toward Your Maximum (And What Doesn't)

Patients often assume that any dental expense counts toward their annual maximum. This isn't always true. Understanding what gets applied to your cap versus what insurance covers separately helps with financial planning.

Typically applied to annual maximum:

- All procedures billed with standard CDT codes (Crowns, root canals, extractions, fillings, implants)

- Diagnostic services (X-rays, oral exams)

- Periodontics (deep cleanings, gum treatments)

- Prosthodontics (bridges, dentures)

Often excluded or paid separately:

- Orthodontia (sometimes has separate lifetime maximum of $1,000-$2,000)

- Teeth whitening and cosmetic procedures

- preventive care in specific plan designs

Some plans pay diagnostic and preventive care outside the annual maximum—a recognition that keeping patients healthy reduces larger claims later. Check your plan documents carefully for this exception.

How to Calculate Your Real Out-of-Pocket Exposure Before Major Work

Before scheduling expensive dental procedures, requesting a pre-treatment estimate is one of the most valuable steps you can take. Most insurance companies offer this service, and dentists routinely provide it for major work.

A pre-treatment estimate (also called a predetermination) tells you:

- What the dentist intends to charge

- What your insurance will pay based on current remaining maximum

- What your actual out-of-pocket responsibility will be

The process typically takes 2-4 weeks, but it transforms an ambiguous financial situation into a known number. For a $3,500 implant procedure, knowing you'll owe $2,800 versus $2,200 is the difference between financial stress and manageable planning.

To get an accurate estimate, ask your dentist's office to submit a pre-treatment estimate to your insurance company before you schedule the work. The estimate is free, non-binding, and gives you leverage to either schedule the work, negotiate pricing, or explore alternative treatment options.

The In-Network vs. Out-of-Network Math

Choosing an in-network versus out-of-network dentist can substantially affect what you owe. In-network dentists have agreed to accept negotiated rates with the insurance company, which are typically 20-40% below their standard fees.

Example: Your dentist charges $2,000 for a zirconia crown. Their contracted rate with your insurance company is $1,400. Insurance pays 50% of the contracted rate: $700. You pay: $1,400 - $700 = $700.

If you see an out-of-network dentist who charges $2,000 for the same crown, insurance may still calculate their benefit based on the $1,400 "allowed amount" but you owe the difference: $2,000 - $700 = $1,300.

That $600 difference in patient responsibility is why in-network dentists are often the financially rational choice for major procedures when insurance is involved.

What to Do Next: Protecting Yourself From Coverage Surprises

Dental insurance will never fully protect you from large dental bills. That's the central reality of how these products function. But you can substantially reduce your exposure through informed planning:

- Know your exact maximum before the calendar year starts. Call your insurance company or log into the member portal. Ask specifically what your remaining annual maximum is and when it resets.

- Time major procedures across calendar years when possible. If you need two crowns and your maximum is $1,500, scheduling one in December and one in January maximizes the insurance contribution across two plan years.

- Get pre-treatment estimates for any procedure over $500. The estimate is free and removes financial ambiguity before you're committed to treatment.

- Compare in-network and out-of-network costs before committing. The difference in your out-of-pocket responsibility can exceed the cost of a preventive cleaning.

- Factor dental costs into any major treatment plan. Before agreeing to implants or full-mouth reconstruction, review our dental implant cost guide and our analysis of root canal costs by region to understand the full financial picture.

Dental insurance is a tool, not a guarantee. Understanding its structural limits—annual maximums, coverage percentages, waiting periods, and the in-network discount mechanism—turns it from an unclear promise into a predictable cost management system. The patients who get surprised aren't those with bad plans; they're the ones who never read the plan documents. Don't be that patient.

Key Takeaways

- Average annual dental maximums in 2026 are $1,500—barely changed from 2015 despite 23% cost inflation

- Major procedures (crowns, implants) are typically covered at 50%, meaning you absorb half the cost plus any excess above your maximum

- Pre-treatment estimates are free and essential for any procedure over $500

- In-network dentists reduce your patient responsibility by 20-40% on average compared to out-of-network

- Waiting periods of 6-12 months apply to major work in most 2026 plans

- Orthodontia often has separate lifetime caps, not annual limits

The gap between what dental insurance says it covers and what it actually pays is measured in thousands of dollars per patient per year. Arm yourself with the numbers before you're sitting in the dental chair.